If you're thinking about equity release, you might be wondering which type of plan is right for you. There are two main options to choose from: home reversion or lifetime mortgage. Both of these plans can help you release equity from your home without having to sell it, but they have different features and drawbacks. Which is right for you?

In this insight, we will consider the features of each and help you to understand which is the better equity release option for you.

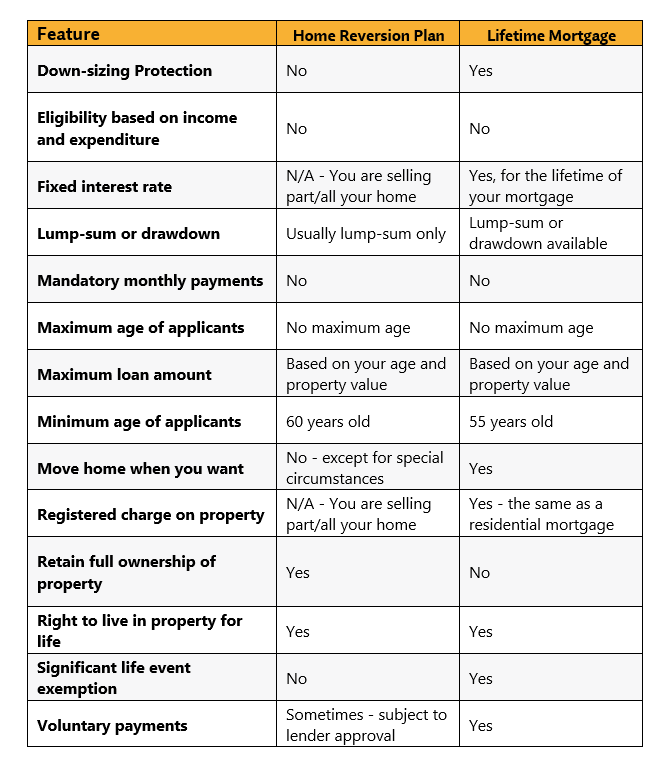

To make an informed decision, let's take a closer look at each option.

A home reversion plan allows you to sell part or all of your home to a lender in exchange for a lump sum or regular payments. You'll still be able to live in your home rent-free, but you'll no longer own the portion of your property that you've sold. This means that you won't benefit from any future increase in the value of your home, and you'll have limited flexibility if you want to move house in the future.

On the other hand, a lifetime mortgage allows you to borrow against the value of your home without selling it. You'll still own your home, and you'll be able to live in it for as long as you like. You won't have to make any monthly payments, but the interest on the loan will accrue over time and will be repaid when you sell your home or pass away.

A home reversion plan means you sell part or all of your property to a company and get money in return. You can still live there without paying rent for your lifetime, but the company becomes the legal owner of the part you sold. When you pass away or move into long-term care, the company gets its share of the sale and you or your family keeps the rest of the property.

Let's say you're a retired homeowner in the UK and you need some extra money to cover your living expenses. You have a house worth £400,000 and you're willing to sell a portion of it to a home reversion plan provider in exchange for a lump sum.

After speaking with a few providers, you agree to sell 50% of your property to a provider for £200,000. You can continue to live in your home for the rest of your life without having to pay rent, but the provider becomes the legal owner of the portion of your property that you've sold.

A lifetime mortgage is a loan secured against your property. It lets you release equity without selling your home. You still own your property, but the lender has a charge on it. This means that you must repay the loan when you die or move into long-term care. Some lifetime mortgages allow you to make interest payments. These can help reduce the amount of debt that grows over time.

If you're 65 and own a £500,000 property but need extra money, you could get a lifetime mortgage for £100,000. You won't have to make monthly payments, but the interest will be added to the loan balance each month. For example, with a 4% fixed interest rate, the loan balance would be £104,000 after one year. The lender will own a portion of the property, 20% in this case. When you die or move into long-term care, the property will be sold, and the lender will receive £100,000 plus any interest. If the property sells for more, your estate gets the remainder after the loan is paid off. For instance, if it sells for £600,000, your estate would get £500,000 plus any interest.

To choose between home reversion plans or lifetime mortgages, consider your situation and preferences. If you want to keep full ownership of your property and are not worried about interest charges, a home reversion plan might work best for you. But if you want to keep full ownership of your property and have the option to make voluntary payments or move in the future, a lifetime mortgage could be a better fit.

It is worth noting that only 1% of applicants now apply for home reversion plans. This is often because lifetime mortgages provide more flexibility.

When deciding, here is what to consider:

With a home reversion plan, you sell a percentage of your home to a reversion company, which means that you will no longer own the entire property. With a lifetime mortgage, you retain ownership of your property, but the lender has a legal claim on a portion of the property's value.

Home reversion plans typically provide a larger lump sum payment upfront, while lifetime mortgages offer the option of regular payments or a lump sum.

Lifetime mortgages have fixed or variable interest rates, while home reversion plans do not accrue interest. This means that lifetime mortgages can become more expensive over time, whereas home reversion plans remain constant.

Both options have age restrictions, but home reversion plans typically require you to be older than for lifetime mortgages.

With a home reversion plan, your estate will only receive the percentage of the property that you still own when you die. With a lifetime mortgage, any remaining proceeds from the sale of the property after the lender is paid off will go to your estate.

Getting the right advice on which equity release option is right for you is critical. Advice is personalised, so it's important to speak with a professional who can understand your unique situation. While there are different options available online, seeking guidance from an expert is essential to find the right solution for you. If you're considering equity release, we strongly suggest seeking financial advice to ensure you make the best decision for your future.

If you're not sure where to start with getting advice, complete the Equity Release Sunny Fact Find. The answers you provide help us to find the best-suited adviser for your needs. Your adviser then contacts you for a no obligation conversation on how they can help. You decide how to proceed.

Stuart is an expert in Property, Money, Banking & Finance, having worked in retail and investment banking for 10+ years before founding Sunny Avenue. Stuart has spent his career studying finance. He holds qualifications in financial studies, mortgage advice & practice, banking operations, dealing & financial markets, derivatives, securities & investments.

(FCA Reg No:604664)

(FCA Reg No:604664)

No minimum

No minimum  Leyland, Lancashire

Leyland, Lancashire SUNNY IN-MAIL

SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:PXK00187)

No minimum

Initial fee free consultation

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:745204)

No minimum

No obligation consultation

(FCA Reg No:NDW01069)

No minimum Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

Free Consultations

(FCA Reg No:571089)

No minimum

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

No obligation consultation

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:PXK00187)

No minimum

Initial fee free consultation

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:745204)

No minimum

No obligation consultation

(FCA Reg No:NDW01069)

No minimum Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

Free Consultations

(FCA Reg No:571089)

No minimum

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

Our website offers information about financial products such as investing, savings, equity release, mortgages, and insurance. None of the information on Sunny Avenue constitutes personal advice. Sunny Avenue does not offer any of these services directly and we only act as a directory service to connect you to the experts. If you require further information to proceed you will need to request advice, for example from the financial advisers listed. If you decide to invest, read the important investment notes provided first, decide how to proceed on your own basis, and remember that investments can go up and down in value, so you could get back less than you put in.

Think carefully before securing debts against your home. A mortgage is a loan secured on your home, which you could lose if you do not keep up your mortgage payments. Check that any mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.

VIEW PROFILE

VIEW PROFILE